Abstract

- One of the most renowned tools to predict future returns as well as ups-and-downs in the stock market is the Shiller P/E, or CAPE (Cyclically Adjusted Price Earnings). CAPE is a 10-year earnings average of e.g. an index relative to the current price. Due to the application of a decade’s earnings, CAPE gives a more accurate estimate of an index or campany’s true earnings power. The S&P500’s CAPE is currently at around 30, which indicates an expected longterm return of 3.3%.

- Any bull market (and subsequent bear market) go through the same stages time and time again. A zeitgeist – spirit of the age – concerning a “new era” drives stock prices to levels where the gap between underlying earnings power and price widens to a degree that smells like a bubble. During this buying frenzy, a feedback loop occurs where market participants drive prices ever higher exactly because of the recent past’s positive price movements. To come full circle, information cascades and excessive confidence lure in more participants, which again drives prices ever higher.

- A period’s zeitgeist, the media’s propaganda, feedback loops and herd behaviour in conjunction leads to irrational exuberance.

Have you ever wondered how stock market bubbles occur? How irrational euphoria lures in the public and ‘forces’ people to jump into speculative ventures despite knowing that the market(s) is/are overvalued? How fortunes are created and destroyed on the back of a “new era” narrative? If yes, you would benefit tremendously from adding Robert J. Shiller’s Irrational Exuberance to your bookshelf. In this awesome book, Robert outlines the many recurring factors and themes that have paved the way for basically all financial bubbles.

The ever-repeating story

When we’re standing face-to-face with a roaring bull market, many recurring factors are staring us in the eye. These are outlined below, but in essence it all comes down to assessing whether the price appreciation is a speculative bubble, defined as an unsustainable increase in prices led by market participants’ buying behaviour, rather than fundamental information regarding value.

This ‘purpose’ is accompanied by a graph that illustrates the S&P500’s price changes relative to underlying earnings between 1860-2000. The graph clearly portrays that the index’ earnings range between $20-$40 throughout the period. The prices, on the other hand, move in a spectrum of $50-$1,500. There is thus a striking discrepancy between earnings power and price movements. The dot-com bubble, where the index reached a P/E of 189, is a dazzling example of how market participants loose their minds and participate in an uncontrollable buying frenzy.

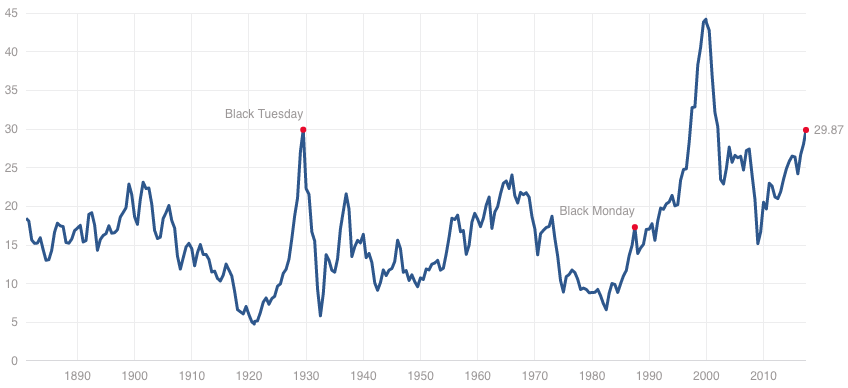

He supports this example with an additional graph containing the four major bubbles: 1901, 1929, 1966 and 2000. Instead of focusing on each year’s price relative to that year’s earnings, Robert applies a 10-year earnings average relative to price. This has later been dubbed the Shiller P/E, or CAPE (Cyclically Adjusted Price Earnings). The application of a 10-year average ‘smooths out’ the earnings and is thus a more accurate picture of an index or company’s true earnings power (just as Benjamin Graham taught us in Security Analysis) relative to price. It’s clear from below graph that the level in 1929 was around 30. At the peak of the dot-com bubble, the Shiller P/E flirted with a ‘value’ of 45.

Take note, we’re currently on the same level as in 1929. Who knows, perhaps the story repeats itself very soon?

The “new era” narrative: The seduction of great stories

What is the ‘ever-repeating story’ exactly? It is, as mentioned, the tendency that stock prices appreciate far more than the underlying earnings power merits. What’s the driving force between the widening of this gap, then? Robert highlights an array of general, recurring factors. The common feature for all bubbles is the creation of a zeitgeist – a spirit of the age, or consensus regarding a “new era”.

In 1901, the “new era” narrative circulated around raging technological development. Railroads, radio transmission, the newspaper industry, the light bulb and the electrograph were all regarded as technological wonders that would change the world. The public, naturally, predicted that these companies would spin gold indefinitely and hence appreciate in value until doomsday. But the bubble bursted in 1907.

The bull market of the 1920s was driven by a narrative of economic prosperity, as described in an article from 1925: “There is nothing that can prevent America from enjoying an era of prosperity beyond compare” (p. 104). Mass production, research departments, large-scale production etc. created a framework for “the industrial and electronic age.” But the bubble bursted in 1929.

The 1960’s bull market’s headline was “new capitalism”, since stocks became common property. Trading stocks was now available to the general public. In addition, everyone was convinced that by investing in stocks, one could “enjoy reasonable, lasting prosperity forever” (p. 110). But the bubble bursted in 1972.

The crusade of the 1990’s was of course ridden under the “Internet”-banner, and how the World Wide Web would change the world of business. But the bubble bursted in 2000.

There might be some merit to George Santayana’s quote: “Those who do not remember the past are condemned to repeat it.”

Feedback loops: Price appreciation breeds price appreciation

A defect in the human psychology can be found in what Robert presents as feedback loops. If we look at a graph of the past’s raging price appreciation, we jump on the wagon not to “miss out” of what one can only extract from such a graph: further price increases. We – as herd animals – acquire more stocks, which results in price increases, which absurdly enough raises the demand. Robert places this tendency within the realm of information cascade theory. The theory dictates that a person observes and copies others’ actions despite that action being in contrast to one’s own beliefs. It is basically the driving force behind herds’ irrational behaviour.

Robert supports this claim via studies that prove investors in the 1990s knew that the market was overvalued, but decided to board the SS Stock Market anyways. Why? The explanation can be found in another emotional defect in our psyche: excessive confidence. The majority of investors answer that they know better than other market participants, which is why oneself is better equipped to beat the market. There is thus a tendency among investors that makes them believe that they can time the market and exit one’s positions before the bubble bursts.

Mix all of these factors with the media’s increased attention on the financial markets who blow-up even minor incidents to hysterical stories, and you got yourself the recipe for a good ol’ fashioned bubble.

Besides these highlights Robert also presents other cultural and psychological factors that affect financial markets to a degree that creates irrational exuberance. I highly recommend this book!

One thought on “Book Summary of Irrational Exuberance”